PODCAST & BLOG

The Four Steps to Selling a Business - Step 4: Closing

By Jay Carter, Founder and CEO, MarketView

The Four Steps to Selling a Business

M&A activity is at an all-time high. The number of transactions is high, valuations are high. Some business owners are approached on a daily basis by eager buyers, hoping their timing is right and the owner is willing to sell their business. With all of this activity comes a lot of confusion-especially for the business owners.

Business owners are business owners. They build and operate businesses. They do not typically buy and sell businesses. So, even though M&A activity is at an all-time high, it’s not for most business owners. Most have still never bought or sold a business and when approached by potential buyers, they are, understandably, uncertain about what to do.

Today, we’re focusing on Step 4 in the sale of a business. This is the fourth of our four-part series discussing the four steps in selling a business. (If you missed previous articles, you can access them by clicking on the links below.)

As a reminder, the four steps to selling a business are:

1. Assessment

2. Improvement

3. Promotion

4. Closing

Step 1 (“Assessment”) is all about understanding what you have to sell and what your goals are for selling it. Step 2 (“Improvement”) involves prioritizing value opportunities previously identified in Step 1 and taking specific steps to increase the value and salability of your business. Step 3 of the business sale (“Promotion”) involves the process of putting the business on the market, offering it to potential buyers, and selecting a buyer to sell your business to.

Step 4 (“Closing”) is the final step in the four-step process to sell a business. To arrive here, you have completed the Promotion step. By this time, you have received multiple offers on your business, negotiated the best deal possible with your preferred buyer, and you have executed a letter of intent (“LOI”).

Once the LOI is signed, you have reached a general agreement on the terms of sale for your business with a buyer, and you will be restricted from marketing your business or talking to other potential buyers until the transaction is either terminated or closed. This period exclusivity generally lasts 60-120 days and is intended to provide time for the buyer to perform in-depth due diligence on the business to confirm that the information you have provided them is accurate and that the business otherwise meets their investment criteria. Final negotiations and legal documentation for the transaction are also completed during this window of time.

This step of the sale process involves close collaboration between your M&A Advisor and your transaction attorney. And it is important that you are represented by an attorney with deep experience working on M&A transactions and also with a reputation for being a “problem solver” vs. a “roadblock”. There are both kinds of attorneys and the former is what you are looking for. Your M&A Advisor should have experience working with numerous lawyers and law firms and should be helpful in recommending one to represent you in the sale of your business.

Surprises come up during due diligence and in final negotiations in virtually every business sale. The best thing an owner can do is to minimize potential surprises by preparing for the sale ahead of time. Most fatal surprises can be avoided simply by completing Steps 1 and 2 of the sale process, but they cannot be completely eliminated.

It is extremely helpful to conduct your own due diligence on your business as part of Step 1 of the sale process and to do a “refresh” internal due diligence just prior to beginning Step 3 of the sale process. This simple process not only re-acquaints you with material that will be reviewed under a microscope by a buyer, but it gives you the clear advantage of entering the market to sell your business. You will have confidence knowing that you are prepared for any buyer’s scrutiny and the results of your efforts will be noticed by the buyer. This will reflect favorably on your business and your management team, and positive impressions are valuable assets during a sale process.

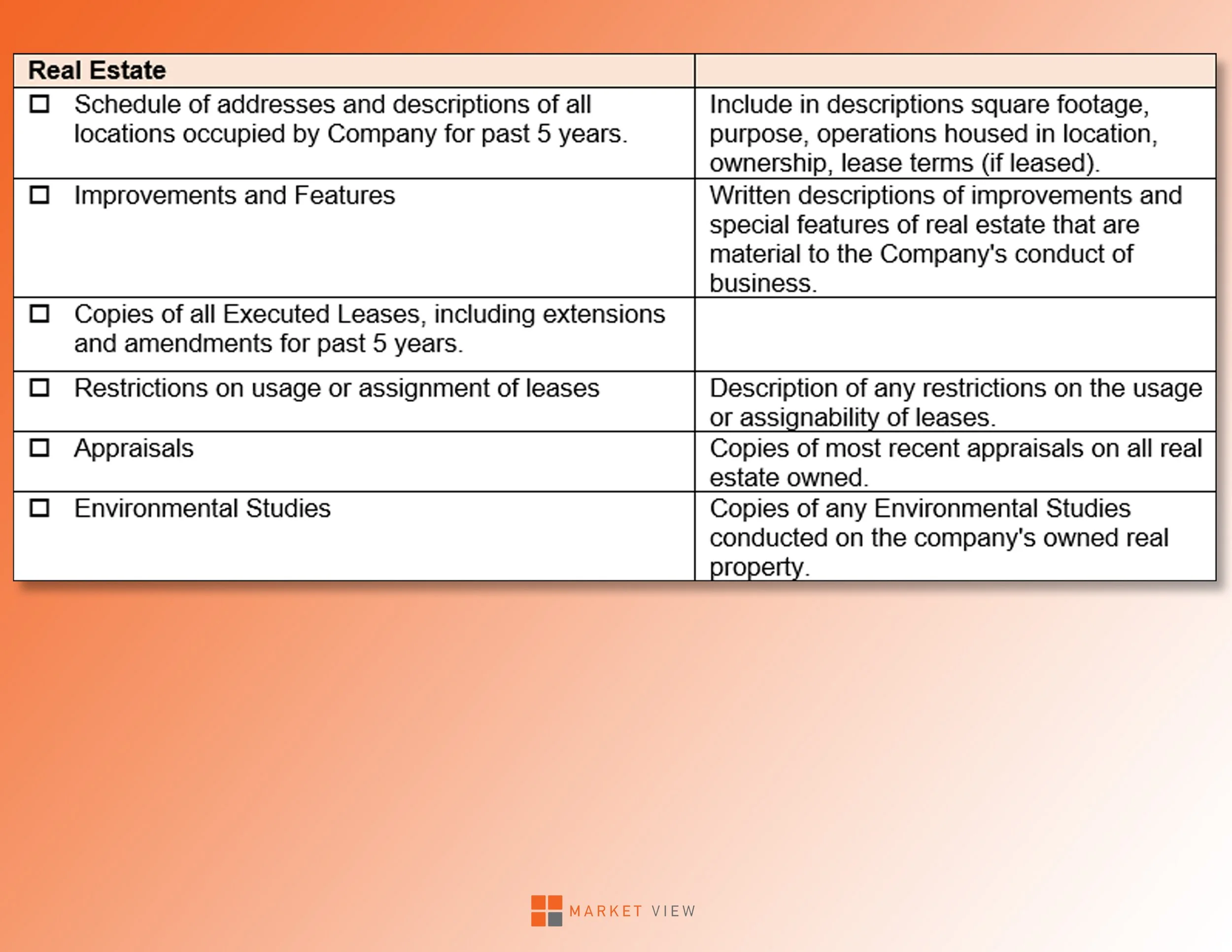

How do you get started with due diligence on your own business? Begin with a good Due Diligence Checklist. The contents of these checklists vary from buyer to buyer and by industry, but the core elements are essentially the same. I have provided our due diligence checklist that you can use for your own purposes at the end of this article. This is a very good checklist to use for pre-transaction planning. Be aware that every buyer has their own checklist which will differ from the one provided here.

With your input, the attorneys and M&A advisors will do most of the work preparing the closing documents. Be aware that some of the terms and conditions contained in the final documents will be different from what you expected. This happens because there are a lot of elements included in closing documents that can not be squeezed into the brief letter of intent you and the buyer signed. Also, new information revealed during due diligence or changes in the business since signing the letter of intent may justify modifications in transaction terms.

Remember that you always have the right to negotiate and challenge unexpected modifications to the deal terms. Your lawyer and M&A Advisor will be able to counsel you on what buyer requests are reasonable and what are unreasonable. Even better, set yourself up to make objective decisions consistently through the sale process. Every business sale is stressful for the owner, especially in the final stages of closing the transaction. To reduce stress and the impact of emotions on your decision-making, there are two things that help tremendously:

1) Know upfront that the final deal won’t look exactly like you expected it to. Changes in deal terms during this step in the process do not necessarily mean that the buyer is a jerk!

Establish your goals for the sale transaction well before signing a letter of intent (during Step 1) and decide then what your minimum acceptable deal looks like. By knowing your walk-away point in advance, you are shifting the timing of this pivotal decision from one of the most emotional and stressful times of your life forward to a time when rational decisions are made, independent of the circumstances of a transaction.

When assembling items in the Due Diligence Checklist, don’t just save the item in a folder and forget about it. Get inside of the mind of the buyer and try to understand why they would ask for this information and what questions they may ask you about it. Anticipate items that may negatively impact a buyer’s perception of the company and address them.

We also recommend that the due diligence items be stored electronically in a secure, cloud-based location, like Dropbox or Google Drive. The protection of the data from being lost or destroyed and also makes it much more convenient to share with buyers in the future.

This concludes our four-part series, describing the four steps to selling a business. It is our mission to empower business owners with the information and guidance needed to have successful exit transactions. MarketView’s process demystifies the sale process and helps any business owner increase the value and salability of their business.

Where are you in the process of selling your business? To receive a free one-hour Sale Readiness Assessment and consultation with MarketView’s founder, Jay Carter, just respond to this email indicating that you’d like to schedule a time. Or, feel free to use this link to Jay’s calendar and find a time now that works best for you. Sale Readiness Assessment w/Jay Carter (Zoom Meeting), or just give me a call on my cell number, below. In this session, we will accomplish the following:

1) We will pinpoint exactly where you are in the four-step sales process

2) We will uncover your top 3 objectives for selling your business

3) We will brief you on current marketplace receptivity for businesses like yours

4) We will provide you with a clear next step for achieving your exit objectives

Sincerely,

Jay Carter

Founder and CEO

MarketView

704-904-7543 (cell)

jcarter@market-view.com